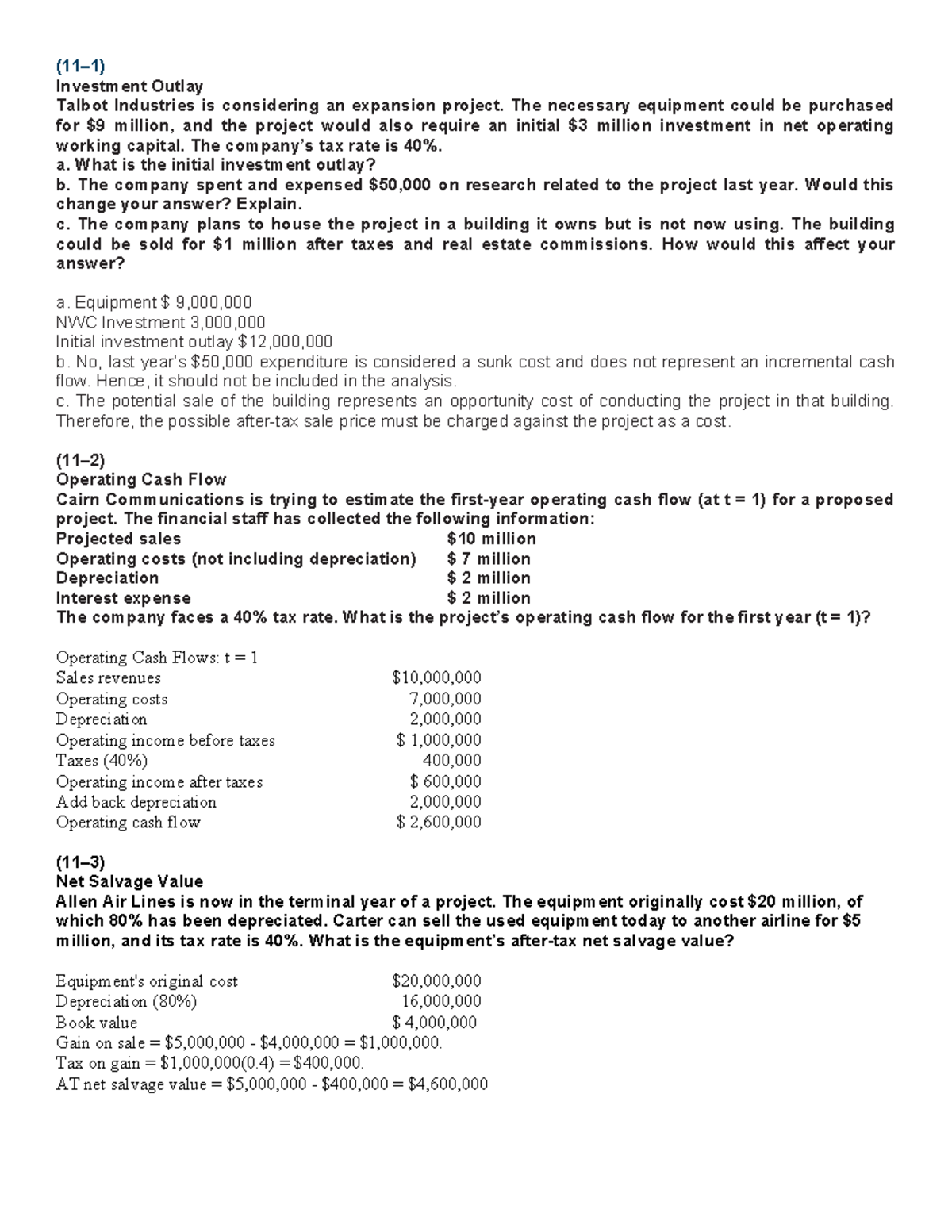

You will find a bank credit card with ?660 balance. This has maximum ?4500, I got this card as 2009. Its inside my label. Anyway the most We previously used is appr ?3k that we repaid for the times, got as a result of ?two hundred, ramped it now to help you ?660. We never ever missed or delay any payment involved. Last night We reduced ?250, harmony is now ?410. I’m gonna pay it off inside the second few days. Anyway a home came toward an industry which we like, could it possibly be really worth to try to get a home loan into the borrowing from the bank cards however unlock? As well as I had a then card having equilibrium away from ?125 ( reduced completely yesterday also) Last thing I have is extremely Account which have Bring 3 option ( pay for the ninety days) I owe all of them ?fourteen this is actually the history fee, along with never skipped people payments prior to.

DH keeps his own mastercard in the label having equilibrium pair thousands but he carefully pays off per month, he is super mindful which have currency. Will it be too early to try to get a mortgage? usually the brand new score enhance? If we enter the mortgage broker work environment to utilize and such he’s going to ask basically have any debts and you will I would personally say, No, as i paid them out of, this won’t let you know for the file as i read it takes days to demonstrate the balance try ?0 even though paid back?

Its good to apply for a mortgage having an equilibrium into your handmade cards. The main thing would be the fact you have never overlooked otherwise come later with a repayment. Communicate with L&C, they’re pretty good and will describe what you to you.

Dont genuinely believe that handmade cards is actually bad. They’re not, they let you know the borrowed funds vendor you pay your debts. if you’ve overlooked a cost (otherwise multiple) that may number against your. Get a better financial coach who’ll help you browse that it

Normal credit card debt that’s paid off and no defaults should make your credit score large perhaps not all the way down. Would you one another enjoys a decent rating, have you ever removed one new borrowing agreements during the last 6 months, do you have one defaults on the data which are not expired or confronted?

I have just adopted a mortgage which have ?3k to the a card (as well as 2 most other notes with zero stability but high borrowing limitations)

I do believe they alters simply how much you can obtain overall, and it’s really a condition out-of my personal home loan that i spend they from towards end (even though my personal advisor says indeed nobody checks!!)

We doubt for those who pay-off now it does show as the a no balance on a credit check, In my opinion they bring a little while to seem?

I looked my rating into Experian past and it’s really 981. In past times eg 2 decades before I became in lot of bills that have ten different credit/ financing storescards, were unsuccessful costs an such like, not I managed to repay all in 2007, even got a mortgage in the 2008 ( sold because that) Now i am cautious not to ever miss payment etc.. I merely borrow what i will pay regarding. Before I found myself more youthful and you will dumb..

Will it counts as I’m lying regardless if I did so spend it well days just before however the borrowing from the bank records hasn’t update they?

We have ?4000 on the a charge card and simply got accepted no issue to own a beneficial remortgage with no credit check payday loans Columbus IL a brand new bank. They’re going to take it off whatever they usually provide you however, around a huge I would perhaps not dump any bed more than.

Okay so now exercise your shared loans in order to income proportion, if it’s under doing 33% you’ll end up great. You’ll probably be great when it is a while over you to definitely centered into the various other bills you possess.

Mumsnet sells particular affiliate marketing backlinks, when you buy something as a consequence of all of our posts, we may score a tiny express of the revenue (info here)